All services Vendor Research

Vendor Research & Benchmarking

Provider landscape research for digital asset infrastructure. Buyers use it to pick. Providers use it to position.

Most digital asset infrastructure decisions still get made on relationships, not evidence. The institutional crypto custody market alone holds hundreds of billions of dollars in assets under custody (Coinbase reported approximately $220 billion in assets under custody at the end of 2024), spread across a small set of regulated providers. The list of NYDFS limited-purpose trust charter custodians is short (Coinbase Custody, BitGo, Fidelity Digital Asset Services, Gemini Trust, Paxos Trust, NYDIG), and the population of CCSS-certified custodians worldwide is similarly small. Yet buyers don’t have good comparative data on who serves which use cases, what features actually differentiate one offering from another, or how published trust signals map to operational reality. There is no Gartner or Forrester for digital asset infrastructure. The traditional analyst-firm model relies on vendor-funded coverage, which collapses in a category where the vendor pool is small and the conflicts of interest are visible. Adjacent research firms (Galaxy Digital Research, 21co, Coinbase Institutional, RWA.xyz, Token Terminal, Glassnode) publish market and macro data, and standards bodies like the Institutional Limited Partners Association (ILPA) and the Standards Board for Alternative Investments (SBAI) frame the buyer-side diligence questions, but none produces buyer-paid independent vendor benchmarking. That is the gap our research practice fills.

How to compare digital asset infrastructure providers

Compare on the attributes buyers actually decide on: key control model, key type, policy capabilities, blockchain coverage, audit and license presence, jurisdiction, and pricing posture. The vendor-paid analyst model that fills this gap in adjacent markets doesn’t exist at scale here, so the comparison has to come from buyer-paid research that uses the products and tracks the evidence behind each feature.

The landscape we research

Digital asset infrastructure is a concentrated market with a clear set of named participants and a clear set of adjacent research providers.

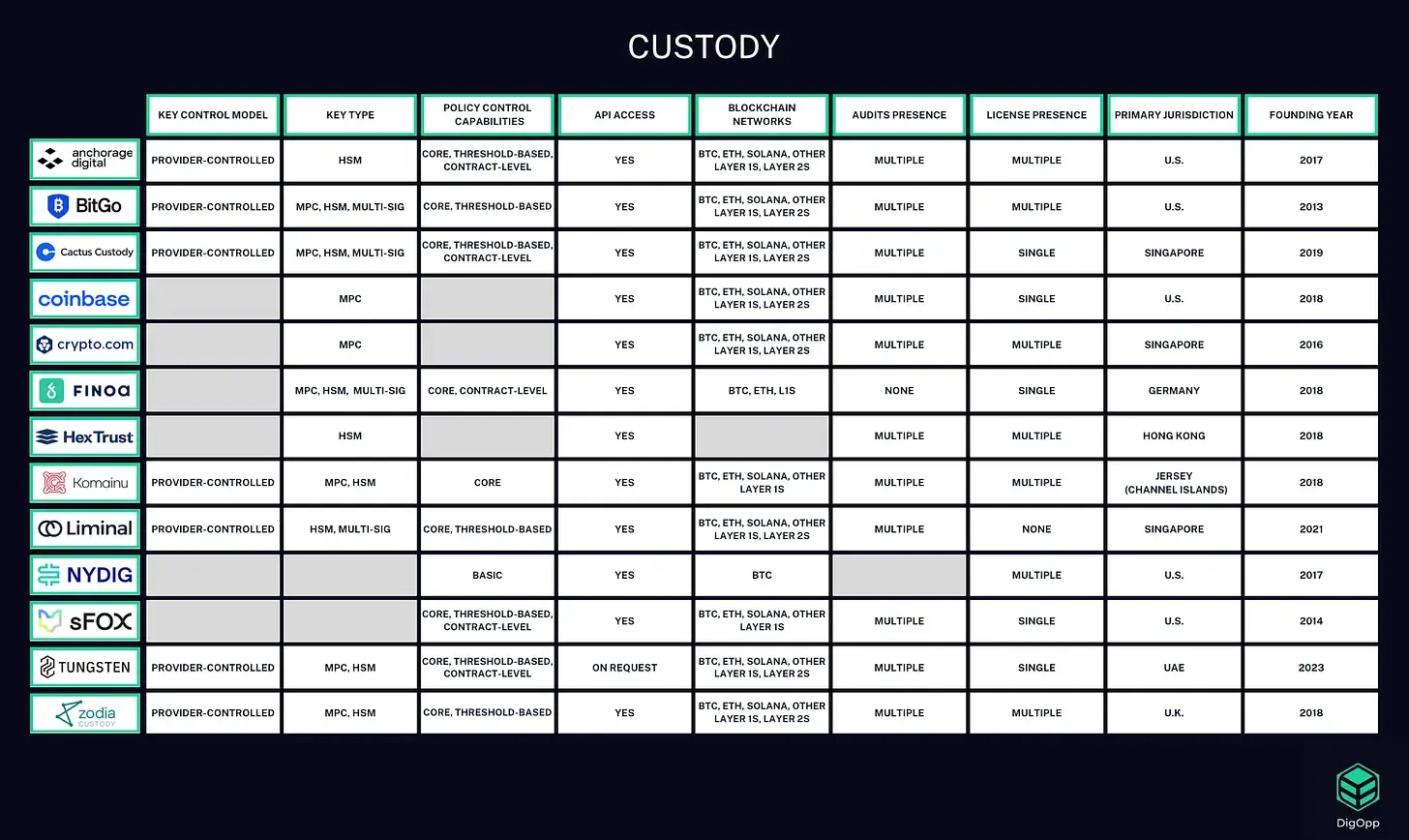

- Institutional crypto custody. A small group of regulated custodians operates under NYDFS limited-purpose trust charters or comparable frameworks: Coinbase Custody, BitGo, Fidelity Digital Asset Services, Gemini Trust, Paxos Trust, NYDIG. Internationally, Anchorage Digital (which received the first federal trust charter for a crypto-native firm in January 2021), Standard Chartered’s Zodia Custody, and Komainu serve similar institutional buyers. CCSS certification (maintained by C4) is held by a small subset of these firms (see CCSS Audit & Readiness).

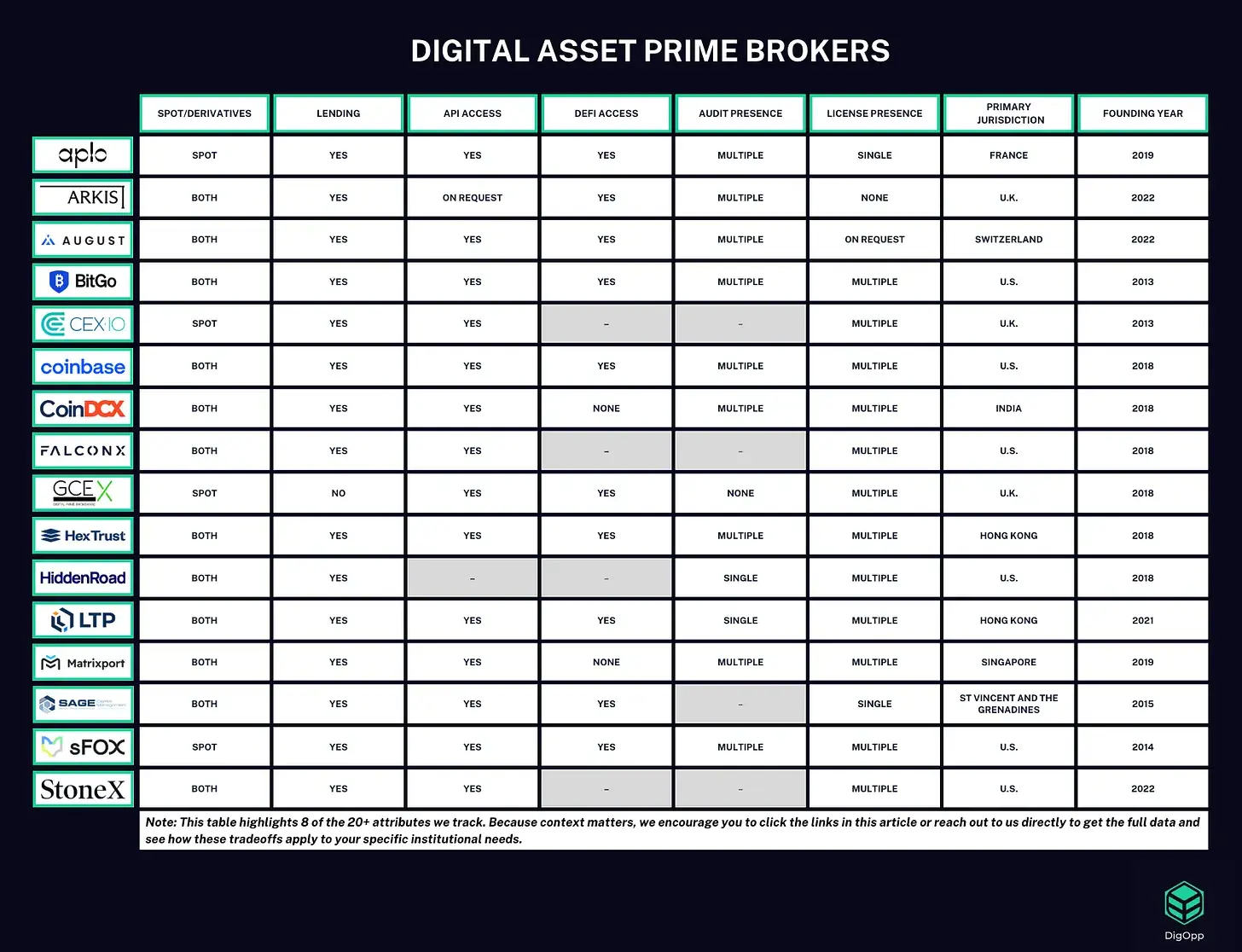

- Prime brokerage, trading, and execution. Coinbase Prime, Galaxy Digital, FalconX, B2C2, Hidden Road, plus tier-one TradFi firms (Goldman Sachs, Standard Chartered) selectively entering the asset class.

- Stablecoin issuers. Circle (USDC), Tether (USDT and the new USA₮ launched January 2026), Paxos (USDP and PYUSD), Ripple (RLUSD), and a growing list of regulated issuers under MiCA in the EU and NYDFS in New York.

- Tokenization platforms. BlackRock (BUIDL), Franklin Templeton (BENJI), Ondo Finance, Securitize, plus tokenized-fund infrastructure providers. Total tokenized US Treasuries crossed $1 billion in 2024 (per RWA.xyz). Boston Consulting Group and ADDX project tokenized illiquid assets reaching $16 trillion by 2030.

- Adjacent research firms. Galaxy Digital Research, 21co, Coinbase Institutional, RWA.xyz, Token Terminal, Glassnode publish market data and macro research; none provides buyer-paid independent vendor benchmarking. ILPA and the Standards Board for Alternative Investments (SBAI) frame the buyer-side diligence questions; SBAI’s 2023 digital asset operational due diligence guide is the closest thing to a shared institutional standard.

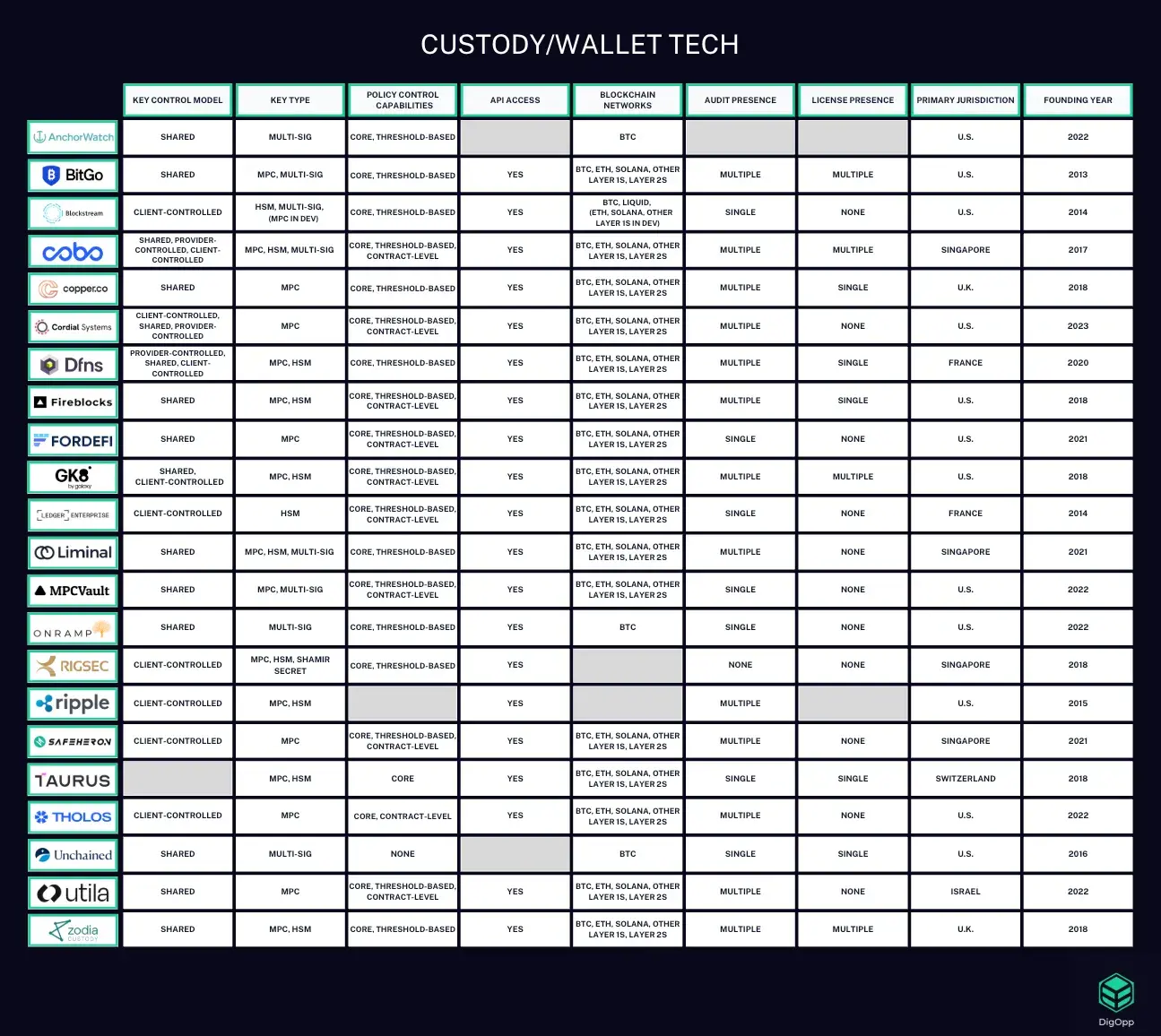

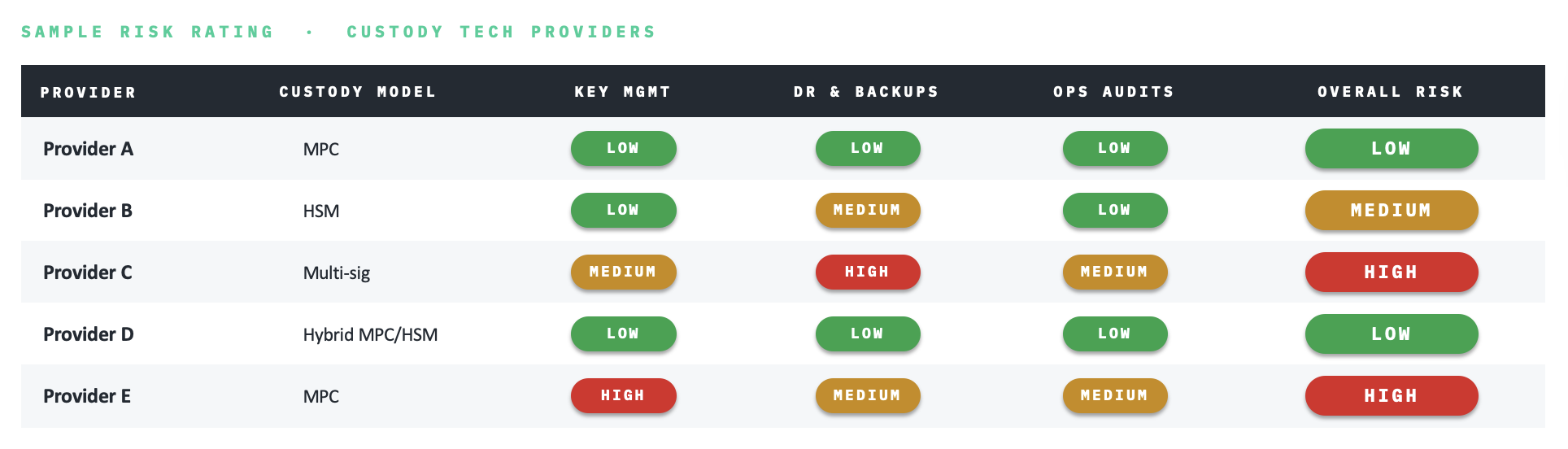

Sample competitive maps from this work

Each map below is the high-level snapshot we share publicly. The underlying research goes further: nearly thirty features per provider, and each feature is a qualitative description, not a yes-or-no field. The columns shown here are the ones buyers ask about first; the report we deliver to clients sits behind them.

A dual-audience research product

The same underlying analysis serves two audiences with different decisions in front of them.

For buyers (institutional clients selecting vendors)

Buyers use the research to short-list vendors and validate features without the noise of vendor-paid analyst coverage. Typical engagements:

- Banks short-listing custodians, prime brokers, or disaster-recovery providers before a vendor selection cycle.

- Allocators short-listing prime brokers or custodians before opening a new line.

- Banks evaluating tokenization platforms before integrating a real-world-asset product (see RWA Tokenization Audit).

For vendors and service providers (understanding their own market)

Vendors use the same research to position against the field, with evidence buyers recognize. Typical engagements:

- Custody platforms raising capital where investor diligence requires defensible competitive positioning.

- Custodians or custody tech providers deciding which features to build to strengthen market position.

- Tokenization platforms pre-launch wanting an honest read on how their design stacks against the field.

Why we are qualified to do this work

- Primary research capability. We have actually used the products we write about. Our research is not a summary of public marketing material.

- Analytical capability. We build data-driven landscape maps, not opinion pieces. Methodology, evidence trails, and source attribution are reviewable.

- No conflicts of interest. We do not resell, distribute, or take referral fees from the providers we benchmark. Our research clients pay us; the providers we map do not. This is a structural distinction, not a positioning claim.

What you get

A research deliverable structured around the question you brought us. Typical scopes:

- Competitive maps. All providers in a category, categorized by service model, feature set, pricing posture, and buyer segment.

- White-space analysis. Where the gaps between buyer demand and supplier capability actually are.

- Buyer-segment mapping. Who uses which provider for what, and why.

- Consumption pattern research. How buyers actually evaluate, contract, and renew in this category.

Deliverables include a written report with methodology, the source-attributed dataset behind it, and an optional briefing for stakeholders.

When to engage

- You are about to build, price, or launch a product and want the competitive picture before you commit.

- You are evaluating a category as a buyer and need a structured view rather than vendor pitches.

- Your board or investors have asked for a defensible view of the landscape.

- You have built something that needs positioning against a field you have not fully mapped yet.

Frequently asked questions

Why is there no Gartner or Forrester for digital asset infrastructure?

The traditional analyst-firm model (Gartner, Forrester, IDC) is built on relationships with vendors who pay for inclusion or favorable placement. In digital asset infrastructure, the firms that could provide this research either have direct vendor relationships, take referral fees, or operate as resellers. The category lacks an independent methodology-driven research provider; that is the gap our research practice fills.

How do you evaluate crypto infrastructure providers without conflicts of interest?

We do not resell, distribute, or take referral fees from any provider we map. Our research clients pay us; the providers we benchmark do not. The methodology, evidence trails, and source attribution behind every deliverable are reviewable. This independence is structural, not a claim.

What does a vendor research deliverable look like?

A research deliverable structured around the question you brought us. Typical scopes: competitive maps (all providers in a category, categorized by service model, feature set, pricing posture, buyer segment), white-space analysis (where gaps between buyer demand and supplier capability actually are), buyer-segment mapping (who uses which provider for what, and why), and consumption pattern research (how buyers actually evaluate, contract, and renew). Deliverables include a written report with methodology, the source-attributed dataset behind it, and an optional briefing for stakeholders.

Who pays for the research, the buyer or the vendors?

Our research clients pay us. The providers we research do not. This is structurally different from the dominant model in adjacent markets where vendors fund their own analyst coverage. The structural difference shows up in what we are willing to say in print, and in which providers we will or will not cover.

How is this different from a vendor's own pitch deck?

A vendor's own pitch deck describes what the vendor wants you to believe. Our research describes what the vendor has actually shipped, against the operational standards institutional buyers actually apply. We have used the products we write about. Most of our methodology is verifying claims against operational reality, not summarizing vendor marketing.

Can vendor research support a board presentation or regulator briefing?

Yes. Research clients regularly use our deliverables for board presentations, investment committee memos, regulator briefings, and competitive strategy reviews. The methodology, evidence trail, and source attribution are designed to support these uses. Where requested, we provide a separate executive briefing or a customized version with redacted detail.

When do I need vendor research and when do I need operational due diligence?

Use vendor research first when the question is the field: who serves what, with what features, at what price, with what trust signals. Use operational due diligence (see [Operational Due Diligence](/services/operational-due-diligence)) once you have a specific target and need to validate its operational design against the controls that should be in place. The two are complementary: vendor research narrows the field; ODD validates the target. Most buyer programs use them in sequence, often six to twelve months apart.

Scope a Vendor Research engagement

Every engagement starts with a scoping call about what you're trying to assure and who you need to assure it to.

Prefer to schedule directly? Book a call

Thanks — your message is in.

We'll reply within one business day. Prefer to talk sooner? Book a call